Personal finance for high earners not rich yet (HENRYs)

Most budgeting advice out there is written for people who need to make every dollar count. That’s not you. You’re earning a good income, but you’re not rich yet. You don’t need to track every single transaction — what you need is a system that protects you from overspending and makes sure your money works for you so you can get rich.

The anti-budget

Tracking every penny is incredibly tedious. Budgeting apps and old-school methods demand too much maintenance, and most of us have better things to do. As a high earner, you need a better approach — the anti-budget.

The anti-budget is simple: you split your finances into three categories:

- Investments: These come first, always. Saving and investing aren’t optional, they’re expenses, just like your rent or mortgage. Every month, a set percentage goes straight into your savings account, Roth, 401(k), or brokerage account. By making it the first thing that leaves your account, there’s no way to “forget” to save. Plus, maxing out these accounts means you could borrow against them later if you need a chunk of cash for something big, like a down payment or a business investment.

- Fixed costs: Rent, utilities, insurance, internet, Netflix, gym membership, etc — these are predictable, recurring expenses.

- Variable costs: Whatever’s left over is for everything else — food, entertainment, hobbies. Spend it how you like, but remember, it’s limited. If you overspend one month and see a credit card balance creeping up, that’s the pain you need to rein it in next month.

The anti-budget is about making sure you’re saving first and spending second. If you focus on these three categories, you don’t need an app telling you how much you can spend on coffee.

Automate everything you can

Pay yourself first

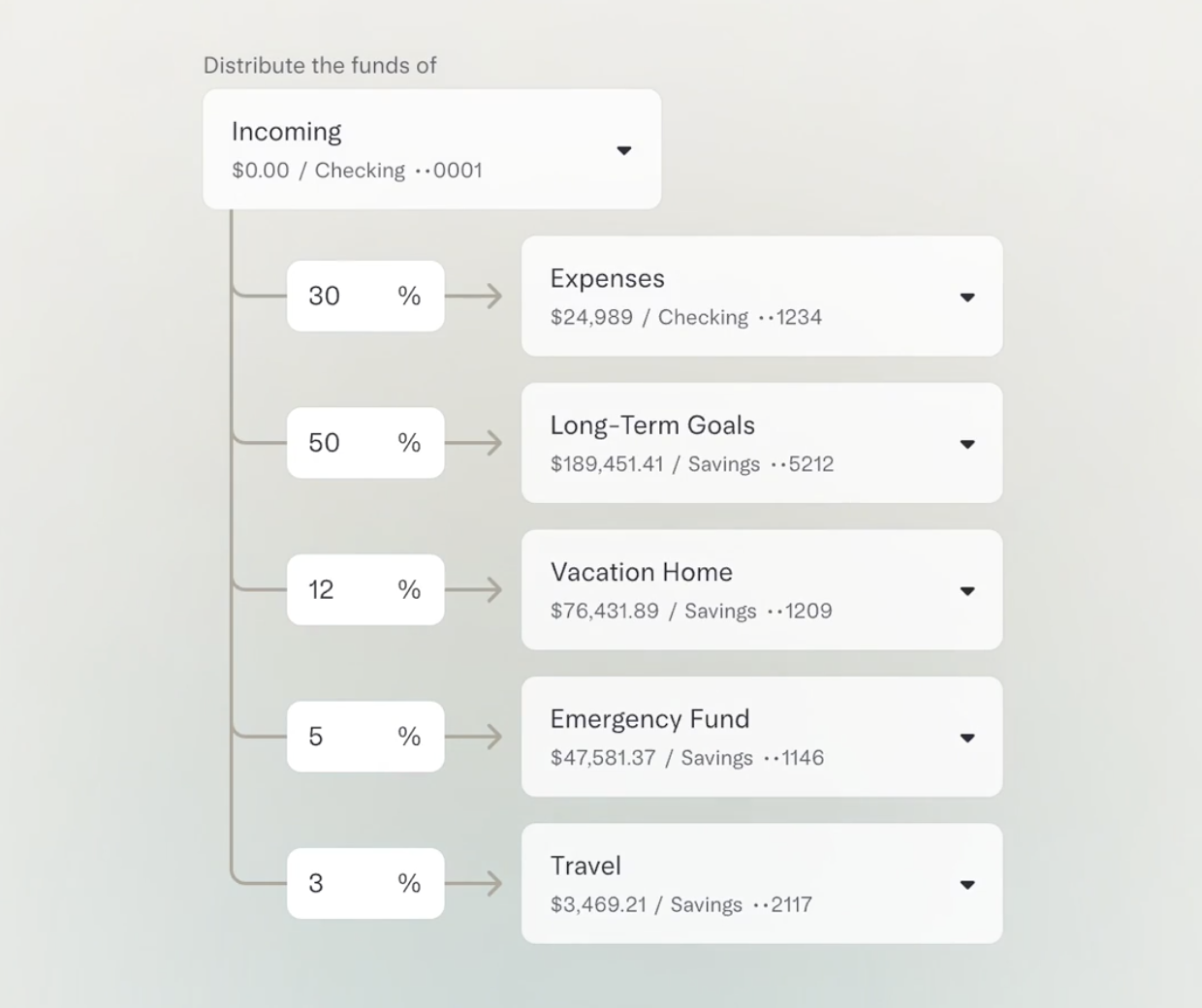

Automate savings and investments to go out as soon as your paycheck hits. This way, you’ll never be tempted to skimp on your future to cover today’s wants. I use Mercury Personal to split money into different sub-accounts automatically. It’s easy to direct a percentage into specific sub-accounts for savings, investments, fixed costs, and variable costs. It can also top off an account that dips below a threshold, so you’re not letting your emergency fund get drained accidentally.

Automate your bills

Rent, utilities, insurance, subscriptions — if you’re logging into anything to pay a specific bill, you’re wasting time. Put it on autopay and it’s one less thing to think about.

Use credit cards to maximize rewards

I put everything on credit cards. This isn’t for everyone — it takes discipline. But if you pay them off every month, you can rake in rewards that cover a vacation every year. I use the Capital One Venture (great travel perks) and Amazon Prime Visa (amazing cash back) for variable expenses and the Chase Sapphire Reserve (huge perk list) for fixed costs. Separating the cards by variable and fixed costs helps keep spending organized and makes it easier to see if the budget’s in line. Plus, keeping utilization low across multiple cards keeps your credit score healthy.

Make your money work for you

Max out tax-advantaged accounts

Put as much as you can into a Roth IRA or 401(k). These accounts aren’t just good for retirement; you can also borrow against them later if you need to, without the typical penalties of withdrawing early. This means the money is still working for you, even if you use it for a major purchase.

I set up a 401(k) through my business with Guideline, which has been great. For personal accounts, I’ve moved everything over to M1 Finance. I’ve also had good experiences with Acorns, Robinhood, Fundrise, and Coinbase.

Build an emergency fund

Ideally, have 3-6 months of expenses set aside. Automate the contributions until you hit the target. This gives you peace of mind and keeps you from dipping into investments when something unexpected happens.

Spend on what brings you joy

You’re earning good money, so spend it where it matters to you. For me, it’s experiences, travel, good food, health, and occasional big purchases that make life better — a new grill, a guitar, a gun. At the same time, I avoid spending on things that don’t matter to me: movie popcorn, overpriced gas, soda, unnecessary upgrades. It’s about maximizing the joy you get from the money you spend.

If you’re a high earner but not rich yet, the key is keeping it simple. The anti-budget makes sure you’re saving first, automating keeps it so you can’t mess it up, and focusing spending on what you enjoy makes it sustainable. When you treat savings and investments as expenses, you’re protecting yourself from the number one threat: overspending. Keep the system tight, stay disciplined, and get rich.

Share this post